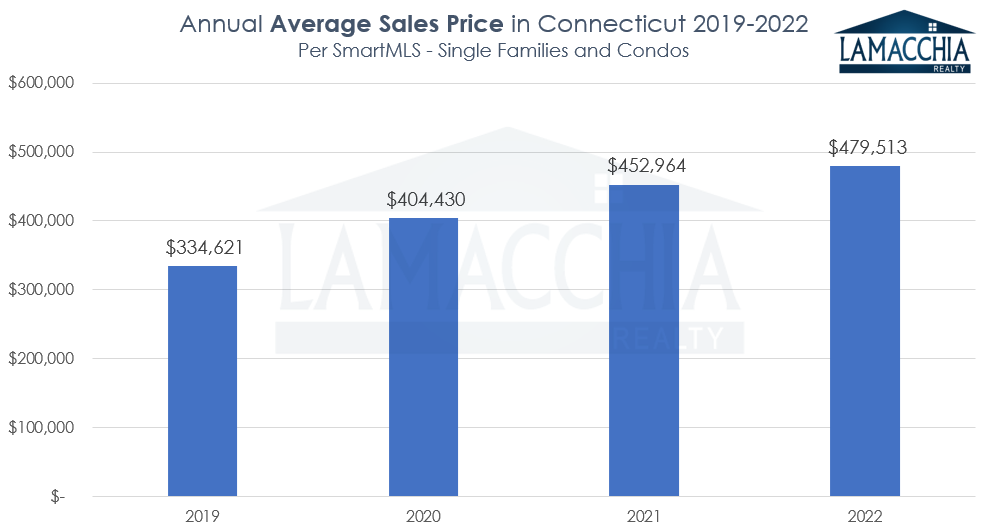

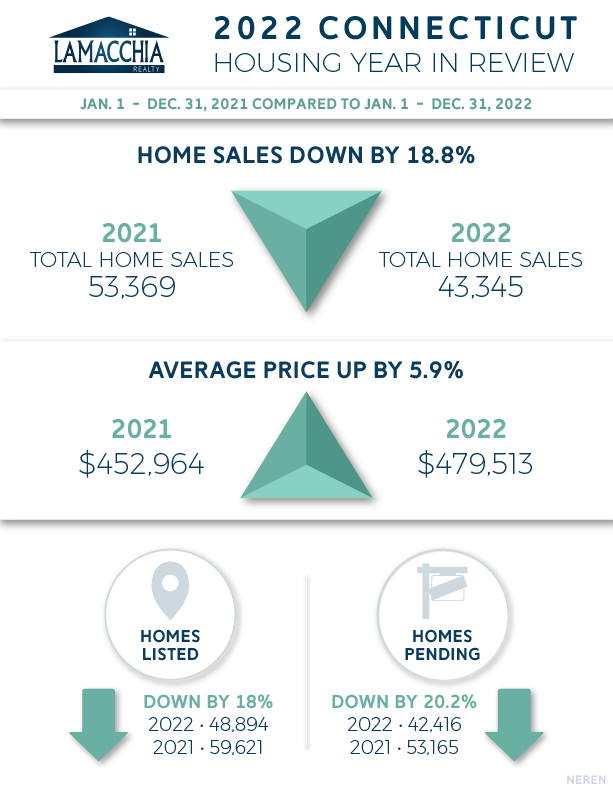

The 2022 Connecticut Year in Review Housing Report breaks down sales, new listings, new pending sales, active inventory, and average price compared to the 2021 market and analyzes what the data means for the current housing market and beyond. In 2022, there were fewer sales in Connecticut than in 2021, down 18.8% overall from 53,369 to 43, 345 in 2022. Conversely, the average price increased year over year, now at $479,513 compared to $452, 964 in 2021, a 5.9% increase.

The 2022 Connecticut Year in Review Housing Report breaks down sales, new listings, new pending sales, active inventory, and average price compared to the 2021 market and analyzes what the data means for the current housing market and beyond. In 2022, there were fewer sales in Connecticut than in 2021, down 18.8% overall from 53,369 to 43, 345 in 2022. Conversely, the average price increased year over year, now at $479,513 compared to $452, 964 in 2021, a 5.9% increase.

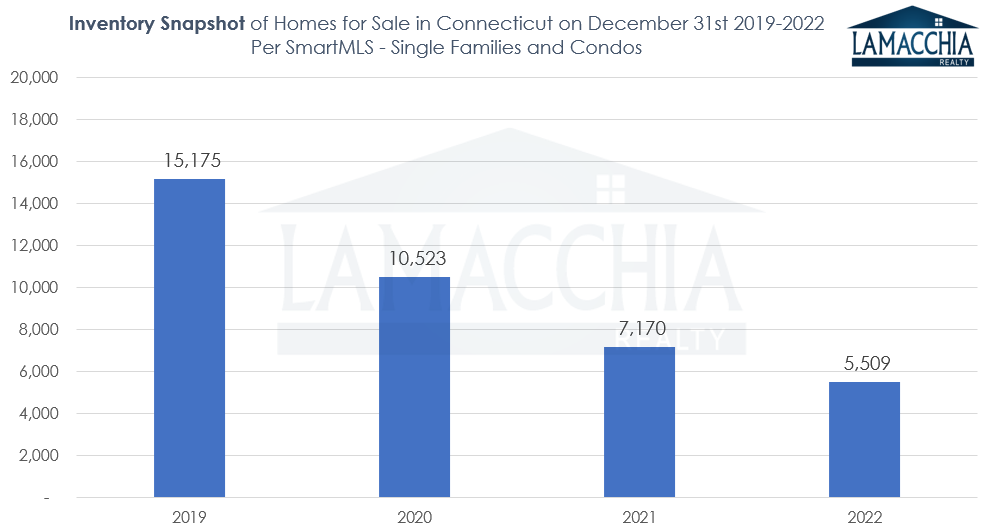

The market trends in Connecticut do not deviate from the real estate story being told nationally, and more of the same is expected to come in 2023, especially in regard to sales numbers. The market was bound to cool and adjust down, as the intense demand coupled with depleted inventory was unsustainable. In 2022, we saw the beginning of that market adjustment, and, as a result, inventory rose a little and the balance between supply and demand (i.e., sellers and buyers) began to restore itself. We also saw average prices slow from their aggressive ascent. This trend is expected to continue into 2023 and Anthony’s explains how this return to balance will look in detail in his 2023 predictions here.